June 2026

- Corbett Road

- Jun 30

- 11 min read

PAY TRANSPARENCY LAWS BY STATE

Pay transparency laws require employers to disclose salary ranges at various stages of the employment process, such as in job postings or upon request by job candidates. They may also prohibit employers from asking job candidates about their salary history. The intent of these laws is to make job searches more transparent and to prevent historical wage gaps from following workers throughout their careers.

As of November 2025, 16 states and the District of Columbia have enacted pay transparency laws, and 11 states have pending legislation.

Source: Paycor, November 2025

LOCKED OUT? HOW TO BREAK INTO TODAY'S HOUSING MARKET

For many young people today, the prospect of buying a home can seem out of reach. High prices, elevated interest rates, and limited inventory all make the current housing market a challenging one. Fortunately, homeownership can still be an attainable goal. It may just take a bit more planning, flexibility, and creativity than it did in the past. Here is a practical guide that can help you navigate the process.

Start with a financial checkup Before you even start looking for a house, you’ll need to assess your financial situation. You should first check your credit score, which is based on your past and present credit transactions. Having a good credit score is important because most mortgage lenders will use it to evaluate your creditworthiness. A higher score will often help you obtain a lower interest rate for a mortgage, which could save you thousands of dollars over the life of your loan. If you discover that you need to increase your credit score, focus on paying your bills on time and reducing high-interest debt.

You should also consider saving for a healthy down payment, since putting more money down can reduce the amount you’ll need to borrow and may make your offer more attractive to a seller. Try implementing the following strategies to help boost your down payment:

Automate your savings so a portion of each paycheck goes directly into a home fund.

Examine your budget and focus on reducing your discretionary spending.

Boost your savings with windfalls from tax refunds, bonuses, or gifts from family members.

Explore first-time homebuyer programs There are numerous mortgage programs geared specifically towards first-time homebuyers that can significantly reduce the upfront cost of buying a home. Government programs, such as FHA loans, often require lower down payments. Local and state programs may offer grants, down payment assistance, or reduced interest rates.

Profile of First-Time Homebuyers

Source: National Association. of Realtors, November 4, 2025

Seek out alternative financing options Buyers can also consider alternative financing options to help lower their interest rates. Here are some that may be worth looking into:

Adjustable-rate mortgage (ARM) also referred to as a variable-rate mortgage, typically has a fixed interest rate at the beginning of the loan, which then adjusts annually or biannually for the remainder of the loan term. The initial interest rate on an ARM is generally lower than the rate on a traditional fixed-rate mortgage, which will result in a lower monthly mortgage payment.

Temporary buydown provides the buyer with a lower interest rate on a fixed-rate mortgage during the beginning of the loan period (e.g., the first one or two years) in exchange for an upfront fee or higher interest rate once the buydown feature expires.

Assumable mortgage allows a buyer to take over a seller’s existing loan and loan terms and pay cash or take out a second mortgage to cover the remainder of the purchase price.

Look into other cost-saving opportunities In addition to alternative financing, there are other ways to help lower the cost of buying a home. One option is to pay an upfront fee at closing, also known as points. By paying points, a buyer can reduce the interest rate, usually by around .25% per point, resulting in a lower mortgage loan payment. Another option, often referred to as a “future refi,” allows a borrower to purchase a home at current interest rates, with the ability to refinance the loan to a lower rate at a later date. The cost to refinance is usually rolled into the new loan, depending on the lender and loan type.

Reconsider what “home” means A first home doesn’t need to be your forever home. Look into smaller properties that tend to be more affordable, such as condos, townhouses, or apartments. Are you priced out of a specific area? Consider emerging and up-and-coming neighborhoods where prices may be more affordable or be open to fixer-uppers if you are willing to invest time (and money) into home improvements.

You may even want to look into purchasing a home with someone else, such as a partner, sibling, or close friend, in order to share costs. While shared ownership can make homeownership possible sooner, it does require trust and clear communication, with clearly documented co-buying agreements, to help avoid future conflicts.

HIGH PRICES FORCE BUYERS TO STRETCH OUT CAR LOANS

In the fourth quarter of 2025, the average monthly payment was $767 for new cars and $537 for used cars. A growing percentage of car buyers are taking out loans with longer repayment periods of six or seven years, which might help someone qualify to buy a more expensive car, but it also pushes up the cost of ownership over time. For example, a borrower with a five-year, $40,000 car loan with a 6.5% APR would have monthly payments of $783 and would pay $6,959 in total interest. A seven-year loan at the same rate would have more affordable monthly payments of $594, but interest payments would total $9,894, an additional $2,935 over the life of the loan.

The typical American wage earner would have to work 36 weeks to pay for the average new car, so it’s no wonder that drivers are hanging on to their old cars as long as possible. The average age of passenger cars on U.S. roads rose to 14.5 years in 2025.

Sources: Experian, State of the Auto Finance Market Q4 2025; S&P Global, 2025

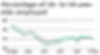

IT'S TOUGH OUT THERE: THE SUMMER JOB MARKET FOR TEENS

Historically, finding a summer job was a rite of passage for American teens. However, over the past 25 years, the summer employment picture has changed dramatically for those ages 16 to 19.

A look back at the employment rate as of July — the peak month for teen summer work — in the 21st century shows a concerning trend: The percentage of employed teens dropped from a high of 44.1% in 2000 to less than 30% in July 2025 (see chart). Despite a gradual rebound after the Great Recession and a slight spike after the pandemic, the downward trend has continued in more recent years.

Reasons for the losses include economic uncertainty, technological improvements, and automation — all of which can reduce business hiring — as well as competition from older workers, teen involvement in extracurricular activities, and, in some cases, a general lack of interest in available jobs.1

Four tips for teens to consider

Nurture and utilize their network. Teachers, friends’ parents, coaches, and relatives may all be great resources who can point teens in a particular direction and introduce them to others who can help.

Build a resume and write compelling cover letters. Even teens who have never worked before can create resumes based on activities, volunteer work, and special school-related projects. The key is to focus on skills learned and experience gained. AI can help craft cover letters that capture attention and focus on skills most applicable to the desired job.

Deliver the application and resume in person, and be sure to follow up. A face-to-face encounter can sometimes help distinguish one job applicant from the many others applying online. A follow-up phone call reinforces interest.

Be creative. Discover other ways to earn money, such as babysitting, mowing lawns, running errands, walking dogs, or reselling clothing and accessories online or in local consignment shops. Cultivating a variety of income streams builds entrepreneurial skills, broadens a resume, and demonstrates resourcefulness to future potential employers.

Source: U.S. Bureau of Labor Statistics, 2026.

1) Challenger, Gray & Christmas, Inc., May 2025

WHAT IS VALUE INVESTING?

During the period before and after World War II, financial analyst and Columbia University professor Benjamin Graham published two books, Security Analysis (1934) and The Intelligent Investor (1949), that defined an approach to the stock market that became known as value investing. Although some of Graham’s ideas have become outdated, his basic strategy remains a bedrock of modern investing, and his most famous pupil, Warren Buffett, is considered among the greatest investors of all time.

Put simply, Graham’s strategy was to analyze the underlying value of a company in relation to its share price and only buy shares of companies that he considered significantly undervalued. He believed that this not only provided growth potential but also what he called a “margin of safety” to help mitigate loss — i.e., he found that undervalued but otherwise healthy companies were less likely to have further large declines in stock prices.1

Becoming a business owner

At the heart of this strategy is viewing the purchase of stock shares as becoming a part owner of a company. “A stock is not just a ticker symbol or an electronic blip,” Graham wrote, “it is an ownership interest in an actual business, with an underlying value that does not depend on its share price.”2 Graham viewed market downturns as an opportunity to buy shares at better values and market upswings as a time to sell stocks that had become overvalued.

Properly evaluating a company requires substantial work and expertise, examining metrics such as earnings per share, the price-earnings ratio (share price/12 months of earnings), and the price-book ratio (share price/net value of company), as well as the company’s operations, market position, leadership, and more. Nonprofessional investors may be unable or unwilling to put in this kind of effort to evaluate individual stocks.

However, there are many funds that focus on “value stocks,” while others may focus on “growth stocks,” which tend to be more expensive in relation to their underlying value but may have more potential for future growth.

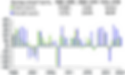

Performance Over Time

The last 20 years have been a strong period for growth stocks, but value stocks outperformed in earlier periods. Annual returns have varied widely.

Source: YCharts, 2026, for the period 12/31/1995 to 12/31/2025. Value and growth stocks are represented by the Russell 1000 Value Total Return and Russell 1000 Growth Total Return indexes, respectively. The performance of and unmanaged index is not indicative of the performance of any particular investment. Individuals cannot invest directly in an index. Investment fees, charges, and taxes were not taken into account and would reduce the performance shown if they were included. Rates of return will vary over time, particularly for long-term investments. Past performance does not guarantee future results. Actual results will vary.

Shifting styles?

Although the principles of value investing are timeless, modern analysts point out that Graham underestimated the growth potential of some stocks that might seem overvalued. This has proven to be true over the last 20 years as large technology companies have experienced rapid growth despite being overvalued by traditional analysis. It’s impossible to know whether or not this will continue, but there was a notable shift from growth to value in late 2025 and early 2026 that some analysts believe could mark a longer-term trend.3

Because value and growth stocks tend to perform differently under different market conditions, it may be wise to hold both types of stocks in your portfolio, which can be accomplished by investing in broad index funds. If you want to weight your portfolio toward a value or growth strategy (often called an investing style), you might add a value or growth fund or individual stocks selected for value or growth. Definitions of value and growth stocks differ among funds and may change over time within the same fund, so it’s important to understand a fund’s objectives and structure.

There is no guarantee that any investment strategy will be successful. The return and principal value of stocks and stock funds fluctuate with changes in market conditions. Shares, when sold, may be worth more or less than their original cost.

Funds are sold by prospectus. Please consider the investment objectives, risks, charges, and expenses carefully before investing. The prospectus, which contains this and other information about the investment company, can be obtained from your financial professional. Be sure to read the prospectus carefully before deciding whether to invest.

1) Investopedia, November 21, 2024

2) Goodreads, 2026

3) Bloomberg, February 4, 2026

WHAT ARE THE TAX IMPLICATIONS OF A SPOUSE'S DEATH?

Losing a spouse is an emotionally distressing time, and not surprisingly, tax-related concerns may not be a priority for a surviving spouse. However, failure to take appropriate steps can lead to a survivor paying more in tax than necessary. Here is an overview of some things the survivor may need to do.

Determine filing status

Selecting an appropriate tax filing status after a spouse’s passing can help manage tax liability. For the year of death, survivors can typically use the married filing jointly status, which may lower tax rates and provide an opportunity to claim more deductions. If the survivor has a dependent child, has not remarried, and meets other requirements, the survivor can use the qualifying surviving spouse status for the following two years. This allows the spouse to maintain favorable joint tax rates while claiming the highest standard deductions to prevent a “widow’s penalty,” which is a tax increase caused by a sudden shift to a single filing status with reduced options for tax breaks. Choosing the right status also may help qualify the survivor for tax credits and determine if a return is even required.

Reevaluate income

The loss of a spouse will probably impact household income. Some income sources may stop, such as employment income, while other sources may start, such as survivor benefits from Social Security or a pension. To help mitigate the “widow’s penalty” and potentially higher taxes, a survivor should evaluate their withholding, estimated payments, and the timing of income and deductions. Adjustments may help prevent unexpected liabilities, manage spending, and minimize taxes through investment restructuring or retirement account planning.

Consider step-up in basis

When a spouse dies, certain inherited assets, such as real estate or stocks, are generally subject to a step-up in basis, which is a tax provision that adjusts the cost basis of an inherited asset to the asset’s fair market value at the time of death. By “stepping up” the asset’s value, capital gain accumulated during the spouse’s lifetime is reduced or even eliminated for the surviving spouse.

For jointly owned property, whether there is a full step-up in basis or a partial step-up in basis depends on the specific ownership type of the property and state law. A tax professional can help with your specific circumstances.

Review retirement accounts

A deceased spouse may have various retirement accounts, such as an IRA, Roth IRA, or 401(k). Unlike real estate and stocks, retirement accounts do not receive a step-up in basis. Instead, their tax treatment generally depends on the type of account, its holdings, and any named beneficiary(ies). A surviving spouse who is named as the sole beneficiary generally has more tax-favorable options than others.*

Plan for gift and estate taxes

Although the federal gift and estate tax may not apply to most estates, surviving spouses with estates exceeding the federal $15 million gift and estate tax exclusion for 2026 should consider consulting a tax or estate planning professional to help manage tax liability. If an estate is less than the exclusion, a survivor may file an estate tax return to elect portability, allowing the spouse to use the deceased spouse’s unused exclusion, potentially reducing taxes.

All investing involves risk, including the possible loss of principal, and there is no guarantee that any investment strategy will be successful. Rebalancing involves selling some investments in order to buy others. Selling investments in a taxable account could result in a tax liability.

*The rules governing inherited retirement account assets are complex, and mistakes can be costly. Distributions prior to age 59½ are generally subject to a 10% penalty in addition to ordinary income tax, unless an exception applies. It may be wise to consult a tax professional before making any decisions.

Spire Wealth Management, LLC is a Federally Registered Investment Advisory Firm. Securities offered through an affiliated company, Spire Securities, LLC., a Registered Broker/Dealer and member FINRA/SIPC.

Neither Spire Wealth Management nor Corbett Road Wealth Management provide tax or legal advice. The information presented here is not specific to any individual’s personal circumstances. Please speak with your tax or legal professional.

These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

This content has been reviewed by FINRA.

Prepared by Broadridge Advisor Solutions. © 2026 Broadridge Financial Services, Inc.